SafeHome.org may receive compensation from some providers listed on this page. Learn More

We may receive compensation from some providers listed on this page. Learn More

The Best Identity Theft Protection Services of 2025

Aura and LifeLock topped our 2025 rankings with their extensive identity and credit protection, generous insurance coverage, and digital safety tools designed to prevent online identity theft.

Max Sheridan, VPN & Identity Theft Protection Expert

Updated February 24, 2025

copied!

Safehome.org is dedicated to helping people rest easy at night. We’re here to show our readers how to get the most secure home possible for the best possible price. That’s why we never charge our readers for our content.

We participate in partnerships that we may receive compensation from. We never allow these partnerships to influence our trusted reviews and rankings.

Our editorial decisions are ours alone, and our recommendations are based solely on our expertise, experience, and opinions. Our reviews are the result of hours of careful research. When we endorse, rank, or review products and services, we’re making independent judgments that you can trust.

In order to keep our important content free to readers, we participate in affiliate programs, including the Amazon Services LLC Associates Program.

Our partnerships exist to help us serve our readers — never the other way around. We partner only with companies that meet our strict standards for quality, and we never allow our partners to dictate the content in our trusted reviews and rankings. Our goal is to deliver comprehensive, accurate, and up-to-date home security information to our readers, and everything that we do is in service of that goal.

Safehome.org is driven by one mission only: to become the #1 resource that helps the everyday person protect themselves and their family.

To this end, we’ve recruited industry experts to advise our editorial team. Our expert panel brings a wealth of experience from various backgrounds such as burglary detectives, identity theft experts, senior care professionals, and more. Rest assured that our reviews, guides, and recommendations all contain factual information from highly-reputable sources.

We also spend countless hours researching and testing products and services. Our objective findings are then distilled into SecureScore, an at-a-glance score that is both trustworthy and incredibly useful.

To maintain reader trust, we must remain unbiased, truthful, and thorough. This is a responsibility we take seriously. We will continue to recruit the brightest minds and deliver top-quality information in each of our reviews and SecureScore ratings. And that’s a SafeHome.org promise.

Best Personal Protection

LifeLock

SecureScore™: 9.6/10

Lifelock comes stacked with real-time threat alerts, robust credit monitoring, and a user-friendly app. It’s not cheap, but Lifelock customers will enjoy a 60-day money-back guarantee and 42% off of their first year of service.

Aura offers comprehensive identity protection and doubles as a VPN to help keep you safe online. It’s not the cheapest option, but you simply can’t beat Aura if you’re looking for robust protection that you can count on.

View Plans

Links to Aura Identity Theft Protection

Most Affordable Identity Protection

Identity Guard®

SecureScore™: 9.3/10

Identity Guard provides comprehensive credit monitoring and identity protection, and also has extra tools, like investment monitoring and home title monitoring. Enjoy up to 40% off on our top-ranked, all-around identity monitoring service for a limited time only.

Protecting your identity is easier than ever with an identity theft protection service. But which one is right for you? We tested the 20 leading options and came up with our own expert-recommended top picks. Here’s the verdict:

Choose Aura if you want extensive protection for yourself or the whole family.

Choose LifeLock if you want identity protection for yourself.

Choose Identity Guard if you want affordable identity protection.

Choose IdentityIQ if you want credit-oriented protection.

Choose McAfee if you want all-around digital protection.

We’re going to expand on those five services in just a little bit, as well as give you five extra options just in case.

Our team has developed a fair and objective way to score the services and products we test. But how exactly did we come up with those scores? Well, the process involves testing out the services ourselves and grading them in terms of customer service, value, features and services, and ease of use. You’ll find our full methodology at the very bottom of this guide.

Here’s what we looked for specifically in every identity protection service we tested:

Identity and credit protection: These two are the core functions of ID theft protection services, and how each service performed in these greatly affected their scores in the ‘features and services’ category.

Monitoring and alerts: As part of our ‘ease of use’ assessment, we looked at how timely and reliably each service delivered alerts. We looked for balance — a service that delivers neither too few nor too many notifications while providing assurance that if someone stole our identity, they’d know and we’d be alerted.

Price and value: Lastly, to assess each service’s value, we looked at how much their identity protection subscriptions cost and how affordable or expensive they were relative to the features offered. We also gave bonus points for free trials or generous money-back guarantees.

Using those metrics, we came up with our top-five picks, all of which have a SecureScore™ of over 9.0 out of 10. Without further ado, let’s meet them!

The Top 5 Identity Theft Protection Services of 2025

Up to $3 million in identity theft coverage per adult

Can be bundled with Norton 360, a high-quality antivirus

Includes alerts for bank account takeovers, and 401(k) and investment accounts

All plans include at least $1 million in identity theft coverage

Quality notifications with helpful descriptions and tips for minimizing exposure

Cons:

Expensive even with an annual plan discount

Only the highest subscription tier includes three-bureau monitoring (the others have just one-bureau monitoring)

Prices increase after the first year

Our Experience:

Why We Like LifeLock

We liked the granularity of LifeLock’s options for individual users. From the entry-level Standard plan starting at $7.50 per month to the Ultimate Plus plan for $19.99 per month, you’re sure to find a subscription that fits your budget and needs. You can even add Norton 360 digital protection to any plan, but it’s optional.

Identity and Credit Protection (9.6/10)

Your identity and credit protection scales with your subscription. We went with the top-tier Ultimate Plus plan so we got the whole nine yards. Besides the usual identity monitoring, we received:

Phone takeover monitoring

Synthetic identity theft monitoring

USPS address change verification

Utility alerts

Data breach notifications

Stolen wallet protection

Plus, we enjoyed credit protection with:

401(k) and investment account monitoring

Buy Now, Pay Later alerts

Credit, checking, and savings account activity alerts

Bank account takeover alerts

Unless you go with the Ultimate Plus plan like we did, you’ll only get credit monitoring for one bureau (Equifax). That’s better than the entry-level plan from Identity Guard (our third pick) that doesn’t offer credit monitoring at all, but we expected three-bureau monitoring from LifeLock’s mid-tier Advantage plan.

Setting up LifeLock took about 10 minutes. It required us to input basic information like name, email, phone number, bank account numbers, driver’s license number, etc. But if you’re going for complete monitoring — and you should — you can add information like your mother’s maiden name, insurance number, and even your gamer tag if you play online games.

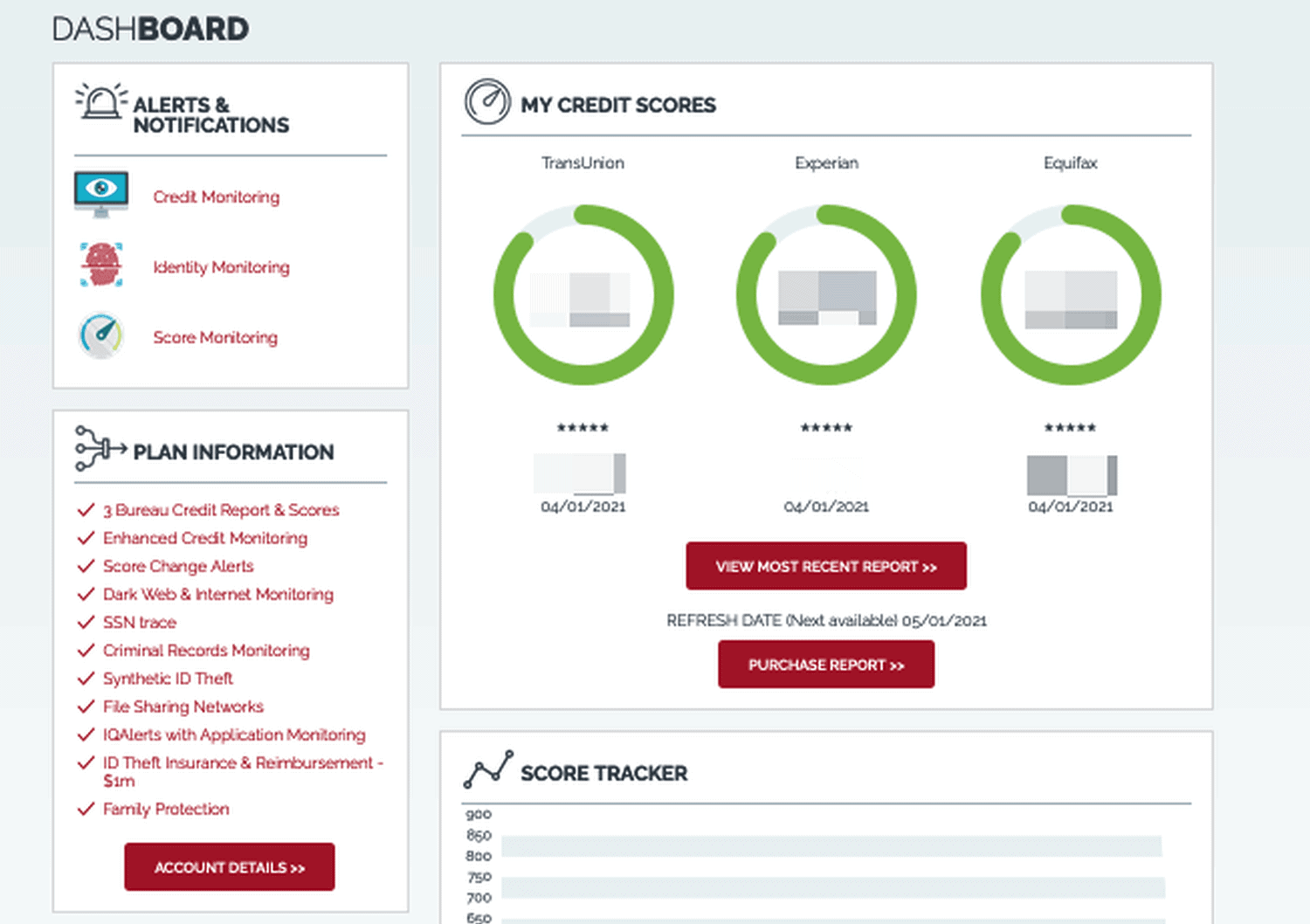

Our LifeLock alerts over the years

As for alerts, they were few and far between. We’ve had a LifeLock subscription for several years now, and we get about two to three critical alerts per year. Unless LifeLock thinks something deserves immediate attention, it won’t bother you. But on the other hand, if LifeLock believes something should be looked at, it makes sure you see it by sending email, text, and app notifications.

Pricing and Value (9.5/10)

LifeLock’s pricing can be confusing, but let’s focus on the individual plans. We encourage you to check out our complete LifeLock pricing page to see what’s in every package.

LifeLock subscription

Standard

Advantage

Ultimate Plus

Norton 360 with LifeLock Select Plus

Norton 360 with LifeLock Ultimate Plus

Monthly billing

$11.99

$22.99

$34.99

N/A

N/A

Annual billing

$89.99

$179.88

$239.88

$69.99

$299.99

One of LifeLock’s downsides is that the subscriptions increase by up to $100 after the first year. Offering a low introductory price is common practice in this industry, but it could throw off your budgeting once the time to renew comes.

On the plus side, it offers a free 30-day trial for all standalone LifeLock subscriptions, and a free 7-day trial for all LifeLock-Norton 360 bundles. Plus, there’s a 60-day refund for all long-term plans, and a 14-day refund for the monthly plans.

All Aura subscriptions include the same core identity and credit protections, so even though we tested the Individual plan, we got a glimpse of how the Family plan works.

Aura monitors a lot. In the identity department, it kept watch of our:

Online accounts

Information on the dark web

Social Security number

Home and auto titles

Our personal information in court and public records

On the credit side of things, Aura gave us:

Real-time, three-bureau monitoring

Monthly credit score updates

Experian credit lock

Monitoring of credit card, banking, and investment accounts

401(k) monitoring

Bank fraud (account takeover) monitoring

Annual credit reports

We also enjoyed active protection from digital identity theft through the Aura antivirus software and VPN, which kept us safe from privacy intruders and data-stealing malware. There’s also a password manager that secures your logins. If you go with a Family plan, you get additional tools packaged in parental control software to help you protect your children’s digital identity.

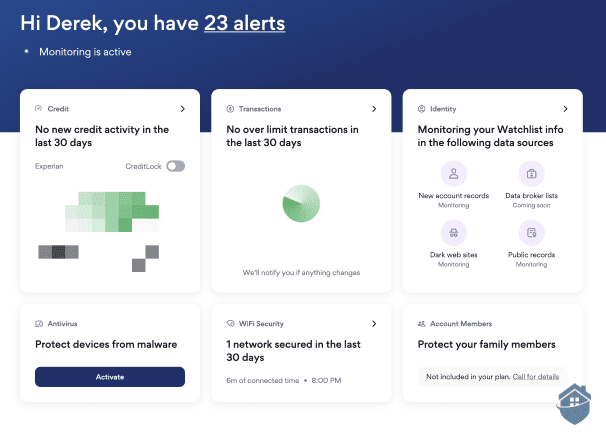

Monitoring and Alerts (9.5/10)

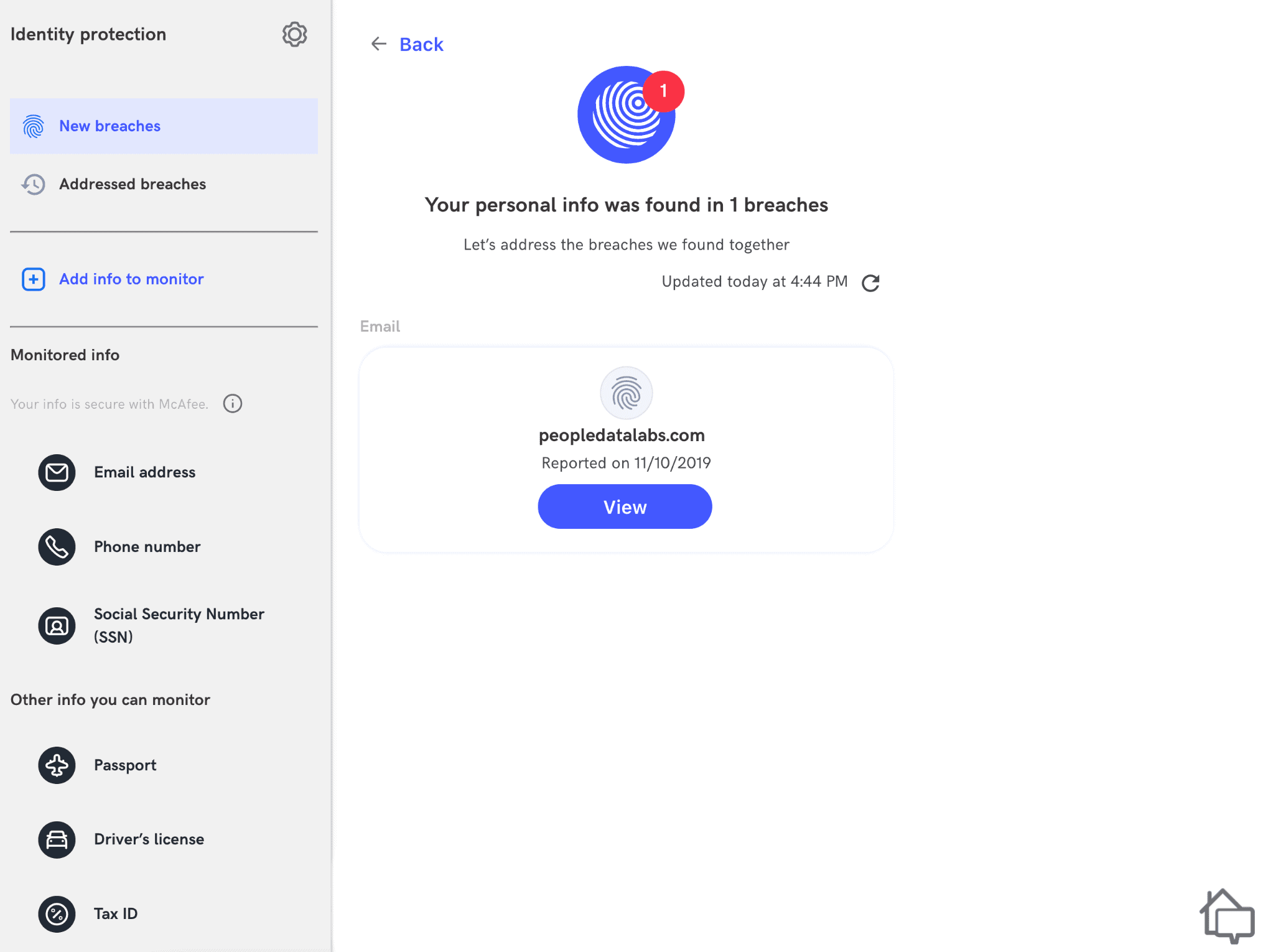

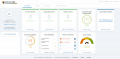

As we added information to our Aura profile, our coverage expanded. It got to the point where we had 23 unread alerts.

Our Aura dashboard with 23 alerts

We recieved those alerts during the setup process, as we were adding information for Aura to monitor. Once we cleared them, we only received relevant notifications, like when we made a big online purchase with our credit card or applied for a mortgage. Overall, we liked the balance there.

Pricing and Value (9.2/10)

Aura subscriptions

Individual

Family

Couple

Kids (add-on to Individual or Couple)

Coverage

1 adult

5 adults, unlimited children

2 adults

Unlimited children

Price per month

$15

$45

$29

$13

Price per year

$144

$240

$180

$120

Annual plan avg. monthly cost

$12

$20

$15

$10

Aura keeps its pricing simple. You go with an Individual, Couple, or Family plan and pay monthly or yearly. Aura tends to be more expensive than other options (Identity Guard starts at $6.67 per month, for example) because the plans are all-in. There are no cheaper tiers with less protection; all Aura plans are comprehensive. Luckily, there’s a 14-day free trial and a 60-day money-back option for yearly plans in case Aura doesn’t pan out for you.

Pro Tip: If your family consists of you, your spouse, and kids, you’re better off buying a Couple plan and the Kids add-on, especially if you plan to pay monthly. The Kids add-on gets you the additional features included in the Family plan, like access to parental control software.

Family plans cover five adults so they can work for small businesses

Tiered subscriptions means you can customize your protection to fit your business

U.S.-based customer service and expert fraud resolution

Near real-time alerts

Cons:

No specific plan for couples

Entry-level Value plan lacks credit and financial monitoring, as well as identity resolution

Total and Ultra Family plans are expensive, at $29.99 and $39.99 if billed monthly

Insurance coverage is the same regardless of the plan

No dedicated fraud resolution service in Value plan

Our Experience:

Why We Like Identity Guard

Identity Guard takes a budget-focused approach to identity protection, especially for those who monitor their own credit. And that’s possible now that anyone can get a free copy of their credit report once a week.1 If you put in the work of monitoring your credit, you can get identity monitoring from Identity Guard for as low as $6.67 per month, complete with insurance, access to a U.S.-based customer care team, and a password manager to help keep your online accounts secure.

Identity and Credit Protection (9.3/10)

Identity Guard can be as simple as Zander Insurance’s entry-level service (one of the cheapest in the industry) or almost as comprehensive as an Aura plan. It depends on which plan you go with. But since Identity Guard is our budget pick, let’s focus on its entry-level Value plan.

Feature-wise, it doesn’t offer much, but that’s expected for its price. For $6.67 per month billed yearly, we got:

Data breach notifications

Dark web monitoring

High risk transaction (e.g. payday loan) alerts

Password manager

$1 million identity theft insurance

U.S.-based customer service

The Value plan is notably missing credit protection. But remember that the $1 million identity theft insurance covers any instance of identity theft, not just the monitored areas. So, if you fall victim to credit fraud, the Value plan gives you just as much insurance coverage as the Ultra (top-tier) plan even though it doesn’t provide credit protection.

Monitoring and Alerts (9.4/10)

We received more notifications from our Identity Guard app than we did from both Aura and LifeLock, but that’s because we were moving some money around during our testing. Two things stood out about Identity Guard’s alerting and monitoring.

First was the speed at which it sent notifications, which was almost real-time. It was so fast that we received a withdrawal alert before we left the bank.

Identity Guard ‘What should I do?” section

Second was the “What should I do?” section that comes with each alert. It provides practical and actionable steps to take. We think it’s a neat feature, since it allows you to react quickly and prevent further damage. You stand a good chance of doing that if you know what to do next.

Pricing and Value (9.3/10)

Identity Guard is our budget pick, but it offers good value plans across the board. That said, the Ultra plan is a touch expensive as it costs more than an Aura individual subscription while offering less protection. It’s still a good pick, but not as good as the Value or Total plan. We also like how all long-term plans come with a 60-day refund. Here are your options from Identity Guard.

All high-ter plans include triple-bureau credit monitoring

Entry-level plan starts at less than $6 per month

Extra security tools, including an antivirus and VPN

Top-tier plan offers identity theft insurance for family members up to $25,000

Cons:

No dedicated family plans

Online dashboard could be made more user-friendly

No free trial and money-back guarantee

Some notifications are delayed

Our Experience:

Why We Like IdentityIQ

IdentityIQ offers one of the best credit protection services we’ve seen. For starters, it offers one-bureau credit monitoring in its entry-level plan, which is priced similarly to Identity Guard’s Value plan. It has three-bureau monitoring in its two upper-tier plans.

We also loved that the two upper-tier plans, Secure Pro and Secure Max, offer additional credit tools like credit score change alerts and credit score simulator, which shows you how big financial moves would affect your credit score.

Identity and Credit Protection (9.3/10)

With credit monitoring being its main feature, our Secure Max subscription gave us one of the broadest credit and financial protection feature sets we’ve seen. The list includes:

Credit score simulation and tracking

Credit score change alerts

Social Security number monitoring

Checking account reports

Utility payment reporting

Monthly three-bureau credit reports and scores

Real-time credit fraud alerts

Expanding on those features, we received identity protection in the form of:

Synthetic ID theft monitoring

Dark web monitoring

Change of address monitoring

Lost wallet assistance

Opt-out assistance (junk mail, Do Not Call lists, etc.)

We would have liked to have seen more features such as home and auto title monitoring like we did with Aura, but we’re confident that IdentityIQ offers enough protection.

Monitoring and Alerts (9.0/10)

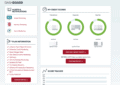

IdentityIQ’s mobile app is new, so we mostly used our online dashboard to monitor our account and make changes. The dashboard isn’t straightforward though. Look at how many panels there are in one page:

IdentityIQ web dashboard

Fortunately, we didn’t need the dashboard to receive alerts. We viewed our action items from it, but alerts came in through emails and texts. That made it easier for us to screen and address them on time, as the alerts themselves contained enough information to let us know if they were urgent. We would love to see a better app though; as of the time of writing, it has a lot of kinks to work out, including delayed notifications.

Pricing and Value (9.6/10)

IdentityIQ has four tier-based subscriptions, and also lets you add an antivirus and a VPN as a paid add-on for just $2 per month (this add-on is included for free with the highest subscription tier). The prices are affordable, but we don’t like how there are no family plans, and how IdentityIQ also lacks a free trial or a refund policy.

Here’s a quick look at all of the provider’s plans:

IdentityIQ plan

Secure

Secure Plus

Secure Pro

Secure Max

Cost per Month

$6.99

$9.99

$19.99

$29.99

Cost per Year

$71.30 ($5.94/month)

$101.90 ($8.50/month)

$203.90 ($16.99/month)

$305.90 ($25.50/month)

FYI: Bitdefender antivirus and VPN costs about $6 per month via the cheapest subscription, but with IdentityIQ you can add both features for about $2 per month.

Full-suite antivirus software, VPN, and password manager included

First-year price averages as low as $5 per month

A.I.-based detection of phishing scams

Up to $2 million in insurance

Offers credit lock

Cons:

Price increases after first year

No monthly billing option; all plans are paid yearly

Apps can be overwhelming as antivirus software, VPN, and other features are crammed into the same software

Family plans are for up to two adults only

Our Experience:

Why We Like It

Our other top picks come with some form of cyber protection, but none of them included a full-featured cybersecurity suite like McAfee did. McAfee included its antivirus software, VPN, password manager, and other cybersecurity tools in its identity protection subscriptions. LifeLock and IdentityIQ only offer cybersecurity tools as add-ons. Compared to Aura and Identity Guard’s complementary antivirus software and VPN, McAfee’s cyber protection is more well-rounded.

Identity and Credit Protection (8.7/10)

McAfee goes all out in the cyber protection department, but it doesn’t offer as many identity and credit protection features as our other top picks. It covers the basics like monitoring the dark web, public records, online accounts, and Social Security number verifications. However, it lacks advanced protections like auto title monitoring, synthetic ID theft detection, and phone takeover monitoring, which Aura and LifeLock offer.

On the bright side, McAfee covers a broad spectrum of credit and financial fraud with credit protection features like:

Three-bureau credit monitoring

Credit lock

401(k), investment, and loan transaction monitoring

Bank and credit card transaction monitoring

Security freeze

Most of those features are available only with the top-tier McAfee+ Ultimate subscription, which is what we tested.

Monitoring and Alerts (9.2/10)

We loved the intuitiveness of the McAfee app, but we felt that it was too crammed with features. All the protections (credit, privacy, malware, etc.) can be found within one app. That made it difficult, at times, to navigate to the feature we were looking for.

Data breach alert from McAfee

Once we got used to McAfee’s app — which took a couple of days — we realized that the features were organized based on the subject they are most relevant to. The VPN was under Privacy, the antivirus software was under Device Protection, and identity and credit monitoring were both in the Identity Column. Overall, McAfee did a great job organizing its app and streamlining the alerting process.

Pricing and Value (9.3/10)

It struck us as odd that McAfee didn’t have monthly plans. Instead, we had to pay upfront for one year of service. Unlike Aura, which offers a 14-day trial and a 60-day money-back option, McAfee provides only a 30-day refund period. These are the options from McAfee:

McAfee+ subscription

Premium

Advanced

Ultimate

For individuals (first year only)

$49.99/year

$89.99/year

$199.99/year

For families (first year only)

$69.99/year

$119.99/year

$249.99/year

FYI: At only $4.17 on average per month, the McAfee+ Premium plan is one of the cheapest options available. But again, you need to pay the full annual price upfront and in the second year, the price will be higher.

Product Specs:

Identity monitoring

Yes

Credit monitoring

1-bureau or 3-bureau

Insurance

Up to $2 million

Free trial

No

Money-back guarantee

30 days

Other Good Options

If you want to continue your search, here are five other services to consider. All these ID theft protection services got a SecureScore™ above 8.0, putting them in the elite class but a tad lower than our top picks. Nevertheless, they offer strong identity and credit protection with unique features you might appreciate.

IDShield (8.8/10)

IDShield offers reasonable pricing with family plans starting at $29.95 and individual plans as low as $14.95. What stands out is the amount of safety net users enjoy — up to $3 million in stolen funds, legal fees, and personal expense reimbursements.

ID Watchdog (8.7/10)

ID Watchdog is a great alternative to IdentityIQ as it offers strong credit and financial protection, especially if you go with the Premium subscription. For example, it monitors subprime loans in your name, high-risk transactions, and can place an initial fraud alert on your credit file encouraging lenders to verify loans applied for with your details.

Allstate Identity Protection (8.6/10)

Allstate Identity Protection does a great job monitoring and protecting identities and credit accounts. But we especially like that it includes home title fraud reimbursement up to $2 million. In addition, it also provides up to $1 million stolen fund reimbursement and $1 million personal expense coverage.

Zander Insurance (8.6/10)

Zander is a budget-friendly alternative to Identity Guard, as personal plans from Zander with only identity protection start at $6.75 with monthly billing. If you go with an annual plan, the average drops down to $6.25 per month. It’s a very affordable option, and still offers decent identity protection.

IdentityForce (8.5/10)

IdentityForce is a great all-around service that offers identity and credit protection as well as safety nets. We recommend it to families, since it has dark web social media monitoring and ID restoration features that cover an unlimited number of children. IdentityForce’s pricing is high, but its features are reminiscent of that of Aura and LifeLock.

What Is Identity Theft?

Identity theft is an umbrella term for different kinds of fraud with one thing in common — the criminal poses as someone else. That could be as sophisticated as using RFID sniffers to lift bank card information from your wallet, or as simple as someone looking over your shoulder at the ATM to get your PIN.

Did You Know? The term “identity theft” was first coined in 1964.

There are various types of identity theft. You’re probably familiar with Social Security identity theft, where a thief gets his hands on your Social Security number to open new accounts in your name, or financial identity theft, where a fraudster fakes your credentials to take over your accounts. But there are other, more nefarious types of identity theft that you might be unaware of.

Types of Identity Theft

Identity theft is as broad as it is complex. Here are a few scenarios you should be concerned about:

Criminal identity theft: This is when a criminal spoofs your identity as insurance before they commit a crime. If they’re caught, they’ll present a fake ID with your personal information. You’ll get a criminal record and if the real criminal makes bail, the police will be after the person they think committed the crime — you!

Estate identity theft: This is where a criminal steals the information of a recently deceased loved one and uses it to open up new credit lines, take out loans, or access government benefits. Since the identity theft victim is deceased, these crimes often go unnoticed and unresolved.

Medical identity theft: This is where a thief assumes another person’s identity to commit insurance fraud or receive medical care using the victim’s name. This one is particularly insidious because it can drive your insurance premiums through the roof.

Identity theft is frightening because most victims do not realize what happened until it negatively affects them, like when they get a call from a collections agency about a debt they were unaware existed. The best thing to do is prevent it from happening in the first place. That means being proactive about your protection. Don’t passively sit by thinking it won’t happen to you.

Did You Know? The odds of becoming the victim of identity theft are about 1 in 15. So it can happen to anyone.

First, pay attention to the warning signs. If something seems out of the ordinary, don’t shrug it off. It could be an indicator that your identity has become compromised.

Second, make sure you’re practicing safe habits both online and in real life. Shred anything that has personal information on it before you throw it away, and be careful when shopping or browsing online. Don’t share your personal information over social media, and make sure you’re using strong, unique passwords on all your accounts.

Finally, consider investing in an identity theft protection service from a reputable vendor, like the 10 we just discussed. The peace of mind these services offer is worth its weight in gold, and their reimbursement and remediation services ensure that should you fall victim, you’ll be able to quickly recover.

What Is Identity Theft Protection?

Identity theft protection refers to a whole suite of services that work to prevent, detect, and resolve identity theft. Features offered by these services often fall under one of these five categories:

Identity protection: Features like dark web monitoring and Social Security number monitoring aim to keep your personal information out of the wrong hands and/or places like dark web black markets where stolen identities are sold.

Credit protection: These protection features focus on your credit file and financial accounts, monitoring for high-risk transactions, suspicious activity, potential account takeover, and so on.

Cyber protection: With identity theft increasingly going digital, cybersecurity tools like antivirus software and VPNs also play a part in preventing digital identity theft.

Insurance: No service can guarantee your protection; in case you fall victim to identity theft, services offer insurance that reimburse stolen funds, legal fees, and personal expenses.

Identity restoration: Lastly, most services offer a dedicated team that users can contact and seek help from in resolving identity theft. Restoration specialists offer various services including assisting in filing reports to the relevant authorities.

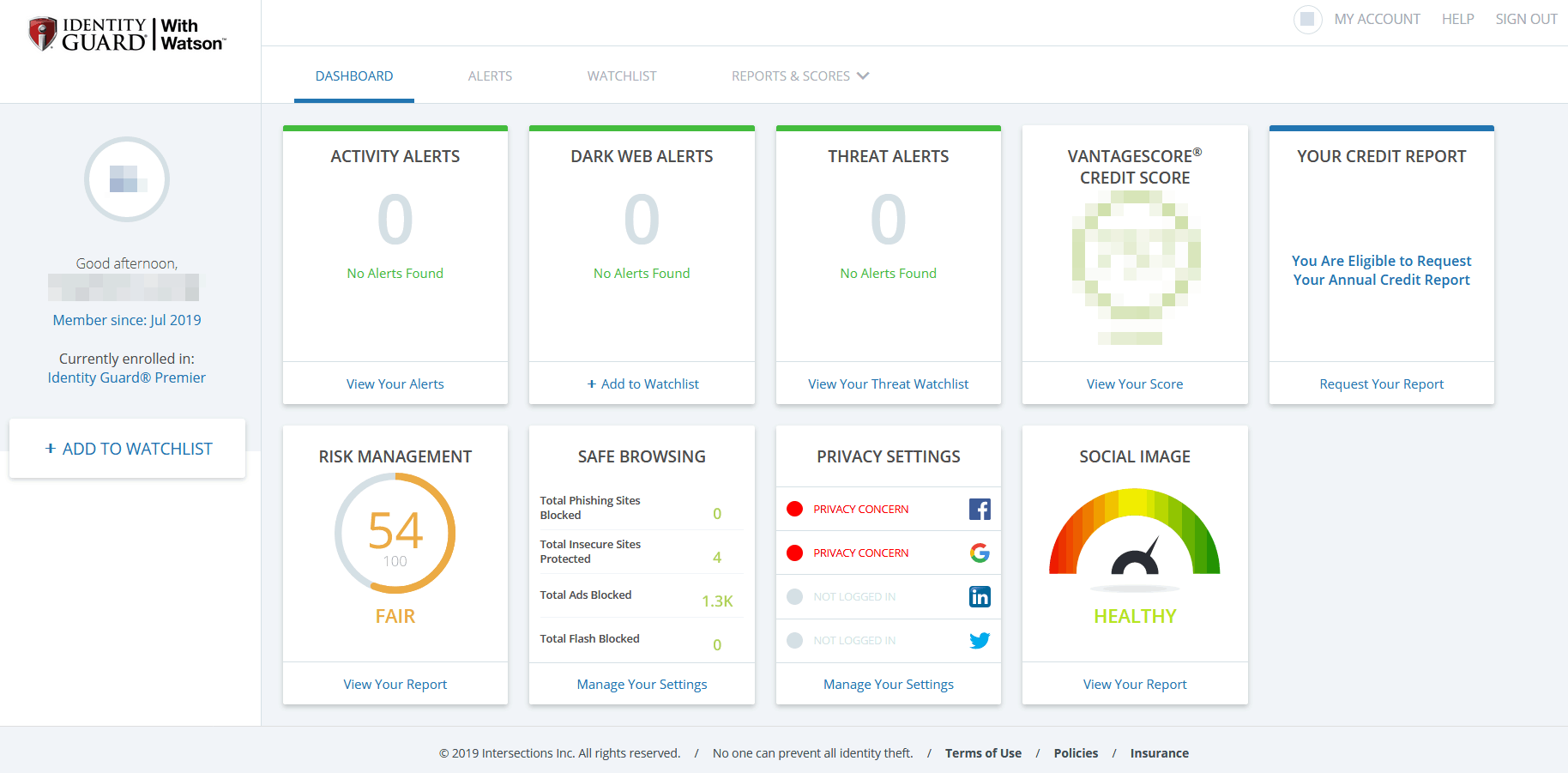

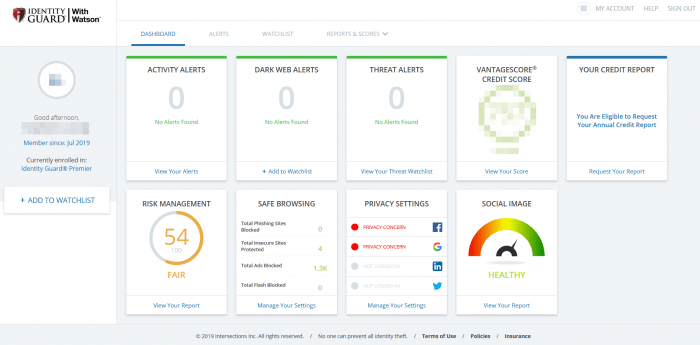

The dashboard of our top-rated Identity Theft Protection Service, Identity Guard.

Many people tune out when they hear the term “identity theft protection.” It sounds complicated and unnecessary, but that couldn’t be further from the truth. The fact of the matter is that identity theft protection is simple to understand. And it’s quite necessary if you want to keep your good name, credit, finances, and other important matters safe and secure.

Unfortunately, identity theft is far more common than most people think. It’s estimated that approximately 10 million Americans succumb to the rising threat year after year. However, there’s really no way of knowing the true number of identity theft incidents, as many victims don’t report their experience to the authorities. This means the real number of identity theft crimes in America might be reaching well beyond 10 million. The bottom line: identity theft is all-too-common.

According to the findings of the National Criminal Justice Reference Service, the most common type of identity theft is government documents and benefits fraud. This accounts for 34% of all reported cases. After that, credit card fraud isn’t far behind, making up 17% of cases. Phone and utilities fraud is the third most common type of identity theft (14%), followed by bank fraud (8%) and employment related fraud (6%), with loan fraud bringing up the rear (4%).

Sure enough, if your identity is stolen, you’ll find out sooner or later. Hopefully it’s sooner, as this gives you time to cancel credit cards, alert credit bureaus, and take other necessary steps to mitigate damage. Here are a few ways you might find out your identity is stolen:

You check your credit and realize your score has suddenly dipped or dropped without explanation

Your credit report shows signs of opened accounts or credit lines, or failed attempts, that you did not initiate

You receive a bill from a creditor that you didn’t sign up with

You suddenly stop receiving mail altogether, signaling change of address fraud

You notice suspicious activity on social media linked to your name

Your name pulls up in court records for a crime you didn’t commit

Although there’s no substitute for identity theft protection services, there are many precautions you can take to protect your identity. Here are a handful of ideas to help you on your way:

Use discretion. Only submit your information on trusted sites that you feel comfortable sharing. Never over-share, and always stop to consider why the website needs the information it’s requesting.

Check URLs. Although you think you’re on Visa’s official homepage, it could be a counterfeit site operated by cybercriminals. Check to make sure the URL in the search bar is official and legitimate.

Only use a secure WiFi connection. This one cannot be stressed enough. When out in public, at cafes and other places, only connect to a secure WiFi signal. This will stop criminals from hacking into your system and stealing your sensitive information as you browse websites, shop online, and interact on social media.

Ensure your computer and other devices are equipped with anti-virus and malware software that monitor threats to keep you safe online.

Shred, don’t toss! Shred any and all documents containing your personal information. Tossing them in the trash isn’t good enough. Criminals will stop at nothing to get their grubby hands on the personal information of others, and that includes digging through the dump.

Monitor your accounts daily. Monitor your bank account, credit card accounts, and credit reports every day looking for suspicious activity. Even if you see a suspicious charge for 50 cents, look into it, as criminals often start small before they drain the account.

Be wary of giving out sensitive information over the phone, especially in public spaces.

Use ATMs with caution. Criminals use a tactic called ‘skimming’ to steal credit card information. If the ATM or card reader looks fly-by-night, keep your card in your wallet or purse. Also, if your card doesn’t easily slide in and out of the machine, do not proceed.

As mentioned above, you can protect your own identity, to a point. For instance, if you find a fraudulent charge on your bank statement, you can call in and have the charge removed. But identity theft protection services go way beyond that by offering everything from SSN monitoring to dark web monitoring, social monitoring, and more. And they even offer impressive insurance policies in the event you need to pay legal fees and the like. These are all things you simply cannot do on your own. To sum it up, you can take basic steps to protect your own identity by being vigilant, but professional services will monitor billions of online data points to keep your name, credit, and finances clean as a whistle. Of course, if you do become a victim on their watch, the service foots the bill to get you back to pre-fraud status.

In the event of financial fraud, the bank will most likely reverse the charges immediately. However, there are several types of identity theft that your bank won’t touch with a ten-foot pole. For instance, the bank cannot monitor your social accounts, your SSN, the dark web, court reports, credit reports, and the list goes on. Bottom line: do not rely on the bank to bail you out of identity theft unless it’s a simple fraudulent charge to your account.

Step 2: Freeze any and all accounts that have been compromised

Step 3: File an official report of the identity theft

Step 4: Contact the credit agencies (Equifax, Experian, TransUnion), notify them of the fraud, and put fraud alerts on your credit report.

Step 5: Continue to monitor your accounts daily

Now, these are the most important steps to take immediately after you become a victim of identity theft. But there are other things to consider, like blocking companies from reporting fraudulent activity on your credit report, reporting the identity theft to local law enforcement as well as the FTC, and contacting your medical care provider to ensure the fraudster isn’t receiving healthcare in your name.

Great question. People often get these three completely different features confused with one another. So this should clear up any confusion.

Identity Theft Restoration — A service many ID protection plans offer that puts a team of professionals in your corner to help cancel compromised credit cards and other accounts, and begin to restore your credit score to pre-fraud status. These services take the reins during an emotionally difficult time. Think home restoration — when a home is restored, it’s not exactly like it was when it was first built, but it’s new and transformed in all the best ways. This feature is not to be missed.

Identity Theft Insurance — A policy of up to $1 million in insurance that covers the steep price of restoring your good name, credit, and finances. For instance, legal fees are covered by identity theft insurance. And good thing, as legal fees can rack up quite the tab pretty quickly. The best identity theft protection services offer $1 million insurance packages, but this varies from company to company. Go with the highest-dollar insurance you can find. (See our ‘Identity Theft Insurance’ section below).

100% Guarantee — A guarantee shows that the identity theft company stands behind their service. Well, sort of. Unfortunately, a ‘guarantee’ is all-too-subjective, and doesn’t have a dollar amount attached to it. If a company ‘guarantees’ to restore your identity, there are typically no mechanisms in place to ensure it happens in a certain time frame, or to the exact specifications that you are happy with. A guarantee is helpful, but don’t stake your entire identity on it. Be sure to also sign up with restoration and insurance.

This form of identity theft happens when a criminal gets a hold of your insurance information. Instead of draining your bank account, they will try to get healthcare, operations, prescription drugs, and other medical-related benefits that belong to you. Of course, nothing in life is free, so when the dust finally settles, the deductibles and claims fall on the shoulders of the victim. The top identity theft services offer medical identity theft protection, which is especially helpful for seniors who use their insurance cards more than the average person.

We read it in the newspaper and see it on TV. A high-profile company suddenly loses half its stock, a large swathe of customers, and its brand image due to a data breach. But what exactly is a data breach? A data breach, data leak, or data spill are three names for the same unfortunate calamity. By definition, a data breach is what you call the unintentional (or intentional!) disclosure of important, sensitive information to an unsecured environment. When the term is used in the context of identity theft, it refers to when a cybercriminal infiltrates or hacks into a database (or other ostensibly protected data source) and steals the information to then use fraudulently. If the criminal does not use the information himself, he will likely sell it or trade it on the dark web. A data breach is a big deal, and the reason why every business should consider an identity theft protection service.

Synthetic identity theft is a new-ish form of identity theft, and considered the perfect, victimless crime by many cybercriminals. Synthetic identity theft occurs when a fraudster creates a fictitious identity from scratch. Fake names, addresses, credit card information, you name it. Sometimes they will create a synthetic identity around one source of legitimate identification, such as a social security number. This type of fraud is especially difficult to track, which is yet another reason why it’s best to leave it to the professionals.

Many of the higher rated identity theft plans include credit monitoring, while others offer it as an add-on for an additional monthly fee. Credit monitoring can absolutely be worth the extra cost, especially if you are looking to buy a home in the near future. Sure, there are ways to check your credit report often, but those will cost you nearly as much as a full-on identity theft protection plan with this feature included. Also, it’s nice to not have to manually monitor the reports yourself. You could miss inquiries, or simply become complacent and forget to check it often. A protection plan that offers credit monitoring will keep a hawk-eye on your credit report, day and night, and send real-time alerts if suspicious activity is detected. So it’s ultimately up to you, but we recommend considering this feature when shopping for fraud protection.

In a word, yes. Identity theft can hurt your credit, especially if it goes undetected. When a fraudster attempts to open lines of credit or purchase big-ticket items using your social security number, it counts as an inquiry on your credit report. With each and every inquiry, your credit score is dinged. It turns from bad to worse if the criminal is approved and they don’t pay the bill (and they won’t pay the bill, promise). If undetected, the account will eventually go to collections, resulting in a massive hit to your credit score, up to 100 points or more. However, if you detect the fraudulent activity in time, you can reach out to the credit agencies to have the activity blocked and the inquiries removed. The best identity theft protection services monitor your credit and streamline the process of getting fraudulent activity cleaned up.

A credit freeze or security freeze is when you ask the credit agencies to completely freeze or block your credit file. When frozen, businesses cannot even check your credit score or report, which means no new accounts can be opened. So when Mr. fraudster is at the Mercedes dealership salivating over that new SLS AMG model, they’ll be met with a hard “NO” when it comes time to get the keys. Many businesses will even alert the authorities when they sense suspicious activity like this. While credit freezes can be helpful at times, they should only be used when necessary, as your credit file is closed to the bad guys and the good guys.

Identity Theft Protection Reviews and Our Process

We have carefully recruited a team of experts in various categories to publish highly-informed, expertly reviewed content.

In this case, our identity theft experts started with in-depth research. They considered industry trends, new products and features, and consumer habits. Then, we had our panel test and review the services to run them through our rigorous vetting process. Our team tested each service for at least a month to get a full understanding of how they worked.

This detailed and intensive review process leads us to our proprietary SecureScore™. The SecureScore™ takes our methodical approach to identity theft protection reviews, and breaks it down into distinct categories, with a score for the following categories:

Through it all, we must research, test, and publish reviews that are of the highest quality. The trust factor cannot be overstated, and trust must be maintained at all costs. That’s why, with everything we write and review, we do it with you in mind.

When it comes to reviewing identity theft protection services, here are the foundational values that we take very seriously.

Objectivity

Reliability

Helpfulness

Honesty

Trustworthiness

Our goal in publishing identity theft protection reviews is to educate you, the consumer, so that you can make an educated buying decision. We want you to find a product or service that fits with your lifestyle and within your budget. In fact, that’s what drives us to become the #1 resource for all things home and personal security.

And we couldn’t be happier to have you along for the journey.

SafeHome.org only uses high-quality sources to support the facts within our articles. Read our editorial guidelines to learn more about how we fact-check and keep our content accurate, reliable, and trustworthy.

Max Sheridan brings over two decades of writing experience to our team. He has spent 1,000-plus hours researching VPNs, identity theft protection, and various topics in cyber technology. Previously, Max was an investigative journalist, and he is also a published novelist. He earned a B.A. in Classics from the University of Virginia and an M.A. in Classics from the University of Illinois. He currently lives in Nicosia, Cyprus.

Updated February 24, 2025

copied!

Updated February 24, 2025

copied!

")