What Is a Credit Report?

A credit report is a document that contains information about your credit activity and current financial situation, including payment histories and the status of your credit accounts. For the most part, these reports are provided by three bureaus — Experian, TransUnion, and Equifax.

Lenders and creditors use your credit report to determine all sorts of things, like gauge if you’ll continue to meet the terms of an existing account or to offer you insurance, rent you a home, or issue you an auto loan. Your credit report can also be used by potential employers to make decisions on whether or not to hire you.

Did You Know? It pays to review your credit report. According to the Federal Trade Commission, one in five reports contain errors.

So, you want to make sure that all of the information on your report is accurate and up-to-date. If it’s not, there might have been a mistake made somewhere along the line, or worse — you might be the victim of identity theft.

When you request your report, it might seem a little complicated at first. That’s okay though, once you know what you’re looking at, things become a little less daunting. Credit reports are divided into four sections, so let’s break those down.

What to Look for in Your Credit Report

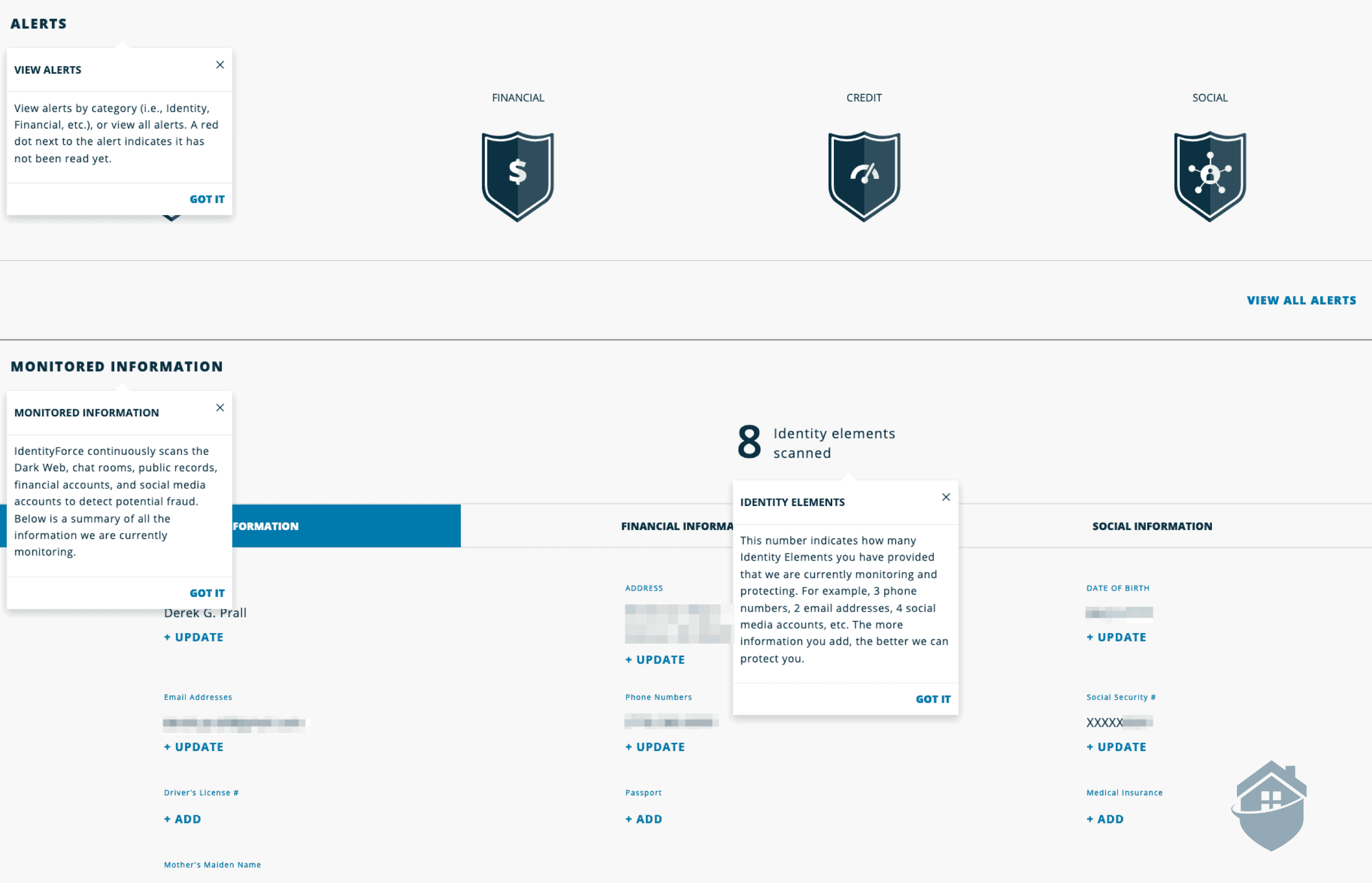

The first section of your credit report is your personal information. This will include your name, any nicknames you go by, your current and former addresses, and sometimes it’ll include your marital status or employment information.

The next section, your credit information — or as they're sometimes called, tradelines — will make up the bulk of the report. This is the information that tells lenders and creditors your history of handling credit accounts. This’ll include a list of your current creditors along with balance information for those accounts as well as payment patterns for the last 24 for 36 months. If you have a late payment or something that has gone to collections, it’ll be indicated in this section.

Next, you’ll find the public records section. This is where anything related to your creditworthiness that shows in your public records will appear. This might include liens, bankruptcies, repossessions, court-ordered child support, or other judgments. Pay close attention to this section. If something doesn’t look right, you’ll want to get it resolved right away.

FYI: Bankruptcy will stay with you for several years, negatively impacting your credit. But bankruptcy is not the end of the world.

Finally, you’ll find your inquiries section. This is a list of anyone who has accessed your credit report. Just so you know, these inquiries can either be hard or soft. A hard inquiry is one that is initiated by you, such as applying for an auto loan. A soft inquiry happens when your report is checked for a reason unrelated to credit applications such as offering you pre-approval for a new credit card.

Most of the time hard inquiries will negatively impact your credit slightly, so you want to avoid accessing your report in this way too often. Be sure to pay attention here. If there are hard inquiries you don’t recognize, it’s a very good indicator that you’re the victim of identity theft.

How To Dispute Something on Your Credit Report

So if you’re being vigilant, you’re checking your credit reports from all three bureaus at least once a year. This will ensure there are no mistakes or fraudulent items negatively impacting your scores.

But what do you do if you find something you don’t recognize? What if there’s something suspicious? Do you have any recourse to dispute your credit report?

Luckily the three major credit bureaus — Equifax, Experian, and TransUnion — have mechanisms in place to resolve disputes. It’s free to dispute an item on your credit report, and both the credit reporting bureau and the information provider (the company or organization that’s giving financial information to the bureau) are legally obligated to respond to your dispute in a timely manner.

Did You Know? If negative information on your credit report is accurate, it could be there for a while. Most negative information will stick around for up to 7 years, and bankruptcy will appear on your credit report for up to 10 years.

While every situation is unique, generally speaking, disputing an item on your credit report is a two-step process: contacting the bureau, and contacting the information provider.

You’ll have to contact the credit bureau in writing with the information you think is inaccurate. The Federal Trade Commission has a sample dispute letter you can use, or you can use the credit reporting bureaus’ online portals:

You’ll need to include copies of any documents that support your case, and clearly indicate which items in the report you’re disputing, and request that the item or items are corrected or removed entirely.

Then it’s up to the bureau to investigate the item in question by reaching out to the information provider for their side of the story. This process usually takes about 30 days, and the bureau will provide you with any relevant information they uncover.

Once the investigation is complete, you’ll receive the results in writing and a new copy of your credit report if it’s changed as a result of the bureau’s inquiry. The bureau can also send updated reports to anyone who requested your file in the past six months, and up to two years if the request was related to your employment.

Did You Know? About 1 in 5 credit reports contain errors, according to the Federal Trade Commission. Thankfully, the best identity theft services offer credit report monitoring and credit score checks so you can stay on top of your creditworthiness.

While all this is going on, you’ll also need to inform the information provider in writing that you’re disputing a piece of information. You can use the FTC’s sample dispute letter if you’d like. Similar to dealing with the credit bureau, you’ll need to include copies of the documents that support your position. They’ll get in contact with the bureau and everyone will be on the same page.

If you suspect you’re the victim of fraud, there will be other considerations — you might need to contact the federal trade commission or the authorities — but more on that later.

How To Get a Free Credit Report

Your credit report is a document containing various data sets that lenders look at to determine your creditworthiness. It absolutely pays to check this report at least once a year to make sure there aren’t any errors and nothing looks out of place.

FYI: Errors on your credit report can drive up your interest rates or you could be denied a loan because of them.

You’re entitled to a free credit report from each of the three major credit bureaus — Experian, TransUnion, and Equifax — every year. You can request your report directly from each agency, or, like the FTC recommends, you can visit annualcreditreport.com to request copies.

Remember, you’ll need your name, address, Social Security Number, and address to request a report.

Keep in mind that reports can be a little confusing if you’ve never seen one before. So now that you know how to get it, here’s what you can expect to find in your credit report.

Lots and lots of information, for starters. The first section includes your personally identifying information, so just make sure that’s all accurate and up to date. Then you’ll move on to the credit account information section. This is where lenders can see your accounts, mortgages, student loan debt or vehicle loans. You’ll also see when those accounts were open, your balances, and your payment history.

Did You Know? Fraud has been on the rise during the COVID-19 pandemic. That’s why Experian, TransUnion, and Equifax are offering free weekly reports. We can’t say for certain how long this will last.

Next, you’ll move on to inquiry information. There are two types of inquiries: soft and hard, and both will show up here. Make sure these inquiries make sense — you’ll see one when you bought your car, for example. If there are inquiries you don’t recognize, it could be an indication someone has or was trying to steal your identity.

Finally, you'll find information on delinquent accounts that have been turned over to collections agencies and bankruptcies. Here’s where you really want to be careful. If anything looks out of place in this section, you’ll want to act quickly to resolve it.

How to Freeze Your Credit

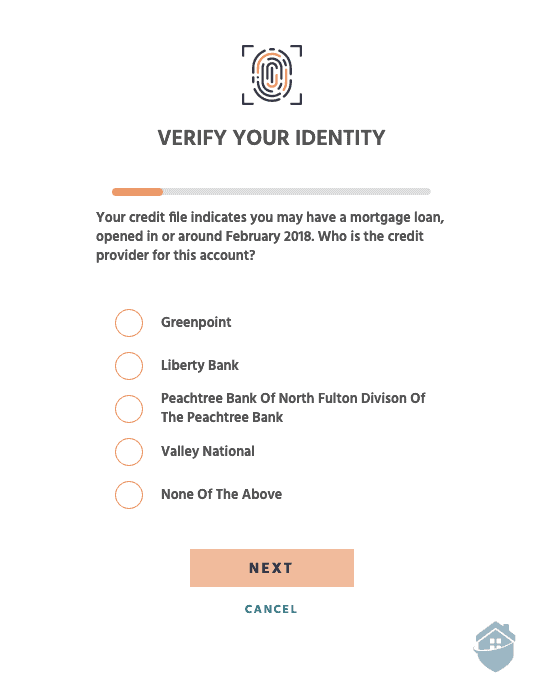

In order to establish a new line of credit or take out a loan, a lender does a “hard inquiry” into your credit file. This helps them determine your creditworthiness — or how likely you are to pay back debt — and will inform their decisions whether or not to issue the loan or line of credit and what your interest rate will be.

Did You Know? Hard Inquiries typically lower your credit score by a few points, but that ding will drop off after two years. It’s not a huge deal if you’re applying for a mortgage or taking out an auto loan, but you might want to think twice about applying for a fist full of credit cards all at once.

Now let’s say someone has stolen enough of your personally identifying information to pose as you and applies for a credit card in your name. The credit card company hard-pulls your report, everything looks good, so they issue the fraudster a credit card. They go on a spending spree, never pay the bill, and when it gets sent to collections, the debt collectors start coming after you.

Nightmare, right? Luckily there are a few ways to prevent this from happening, namely credit freezes and credit locks.

Generally speaking, credit freezes and credit locks accomplish the same thing. They prevent creditors and lending agencies from accessing your credit files, and, by extension, prevent unauthorized parties from taking out loans or establishing lines of credit in your name.

Federal law gives you the right to activate and remove credit freezes from each bureau for free. You’ll have to contact each credit bureau individually — Experian, TransUnion, and Equifax — to request them to freeze your credit file. In most cases, this can be done electronically.

Each credit bureau is required to place the freeze within 24 hours of your request, and they’ll provide you with a PIN you’ll need to unfreeze your file. The freeze must be lifted within one hour of request with the provided PIN. Just FYI, though, if you lose the number you can be issued another, but it will take much longer to unfreeze your file.

Locks differ from freezes, but only slightly. They accomplish the same thing, but locks are set and lifted in real-time. Locks are usually set up through third-party vendors like identity theft prevention products or through a secure website or app provided by the credit monitoring bureau. To set up a lock through the credit monitoring bureaus, you’re going to need proof of identification that can be submitted electronically or via hard copies.

How to Check Your Credit Score

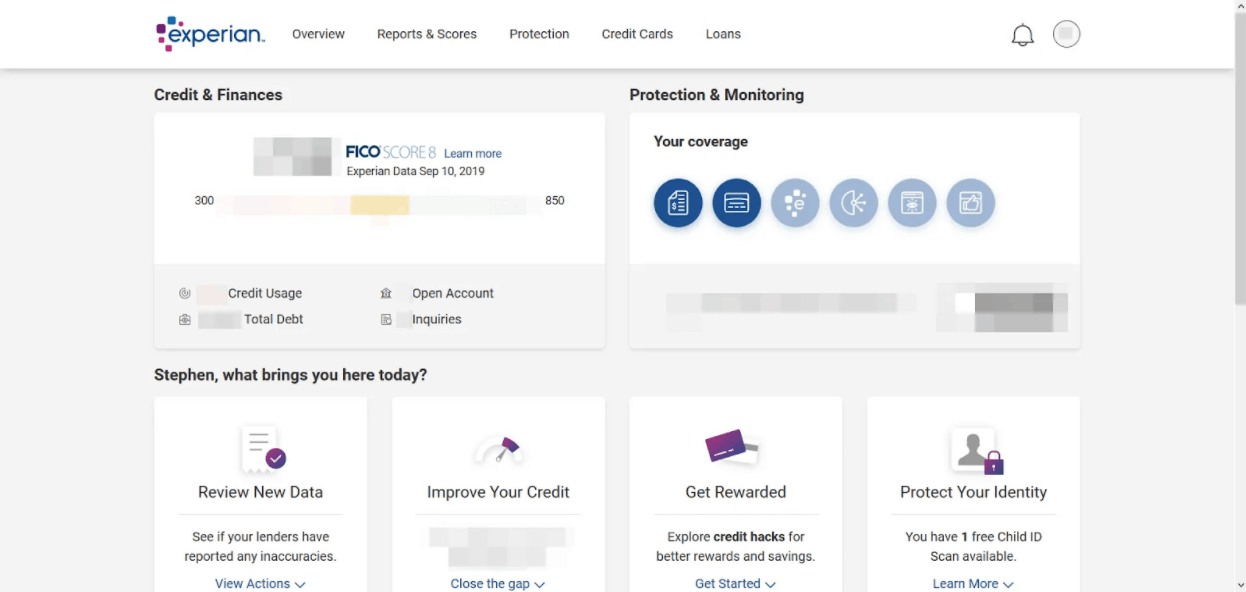

Your credit score is a three-digit number that reflects your creditworthiness based on your credit history, payment patterns, and current debt levels. In simple terms, it tells lenders how likely you are to repay borrowed money.

Higher scores signal responsible financial behavior, often resulting in better loan terms, higher credit limits, and lower interest rates. That said, each lender evaluates applicants differently, and your credit score is just one factor in their decision-making process. Generally, scores fall into categories from “Poor” to “Excellent,” helping both you and lenders understand your financial standing at a glance.

Credit Score Breakdown

- 300-579: Poor

- 580-669: Fair

- 670-739: Good

- 740-799: Very good

- 800-850: Excellent

In the U.S., three main credit bureaus — Equifax, TransUnion, and Experian — calculate credit scores using slightly different methods and data points. The most widely used model is the general-purpose FICO score, though industry-specific FICO scores and alternatives like VantageScore exist.

Did You Know? It’s perfectly normal for your scores to fluctuate slightly between the three bureaus. While they all use similar data sets, they sometimes weigh specific indicators differently.

Everyone is entitled to a free credit report from each bureau once a week, though these reports typically don’t include your actual score. To access your score, you have several options: check with your bank, credit card, or lender; request it directly from the bureaus (small fees may apply); or use online services, some free and some paid.

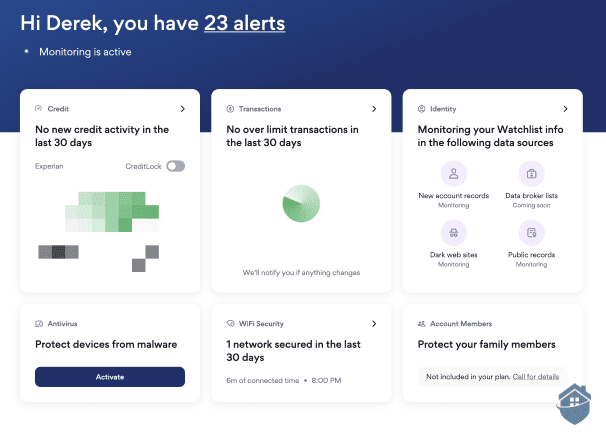

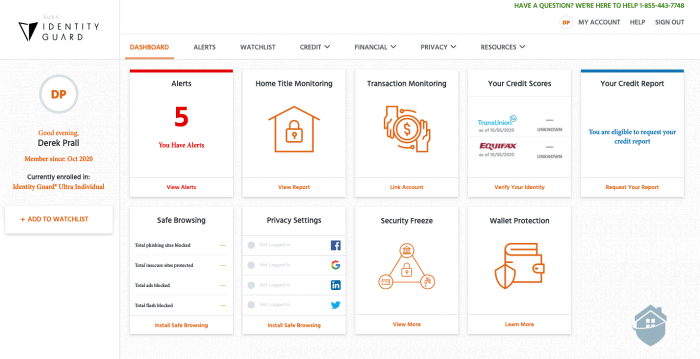

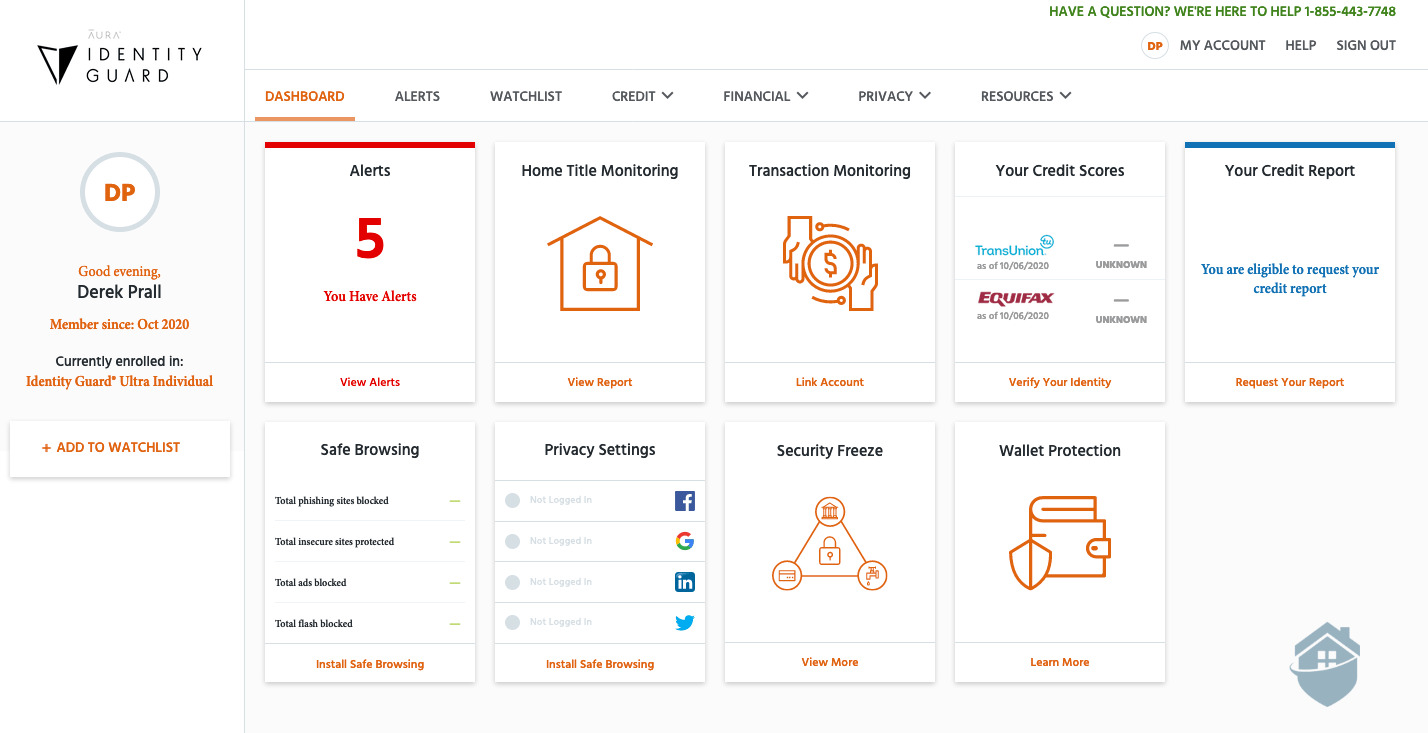

In our experience, the best approach is to use a reputable identity theft protection service. Services like Aura, IdentityForce, LifeLock, or Identity Guard provide real-time access to your credit scores and alert you to significant changes.

Monitoring your credit isn’t just about loans or interest rates — sudden drops in your score are often the first sign of identity theft. Early detection lets you act quickly to minimize damage and protect your financial future.

FYI: Want to find coverage that includes restoration if you happen to fall victim to fraud? If so, read our guide to the best identity theft protection with restoration. You’ll find that these plans all come with up to $1 million in identity theft insurance, dedicated restoration resources, and other benefits should you be targeted by fraudsters.

Features of Identity Theft Protection Plans with Credit Monitoring

The following are the most common features of identity theft protection services that include credit protection:

Bank Account Takeover Protection

Account fraud and credit theft go hand-in-hand. And bank account takeover is a serious matter — one that must be combated with a serious solution. The fraudster’s aim is to hack into your account and drain your net worth. So many ID theft services with credit monitoring offer this anti-takeover feature that keeps criminals out of your accounts.

Payday Loan Monitoring

Identity theft services with credit monitoring sometimes offer Payday Loan Monitoring. This feature searches for your name across high-interest loan companies. In the event your name is detected, it’s flagged and you will receive an automatic alert. Taking out loans in someone else’s name is a typical tactic for criminals.

Credit Report Monitoring

Most services that offer credit monitoring also offer credit report monitoring. With this feature, your credit reports from the three main bureaus are under constant monitoring. If there’s even a hint of suspicious or unusual activity — or any inquiries or changes to your credit whatsoever — you’ll be immediately notified.

Identity Theft Insurance Coverage

Signing on with just any service with credit monitoring doesn’t mean you’re 100% safe. Fraud still happens. So the smart move is to get covered with identity theft insurance. Some companies put their money where their mouth is with an impressive $1 million policy. This feature could help to bail you out of attorney fees, stolen funds, you name it.

401(k) and Investment Activity Alerts

You saved your whole life. You do not want your savings wiped out in one ruthless act of fraud. To avoid this, find an ID theft protection service that offers credit monitoring and 401(k) and investment activity alerts. This suite of features monitors your accounts for suspicious activity and sends automatic alerts if foul play is detected.

Bank and Credit Card Activity Alerts

A critical feature to say the least, these alerts are triggered when a bank withdrawal, transfer, charge — or really any activity — deviates from your pre-configured settings or dollar amounts.

Loan Application Monitoring

Identity theft protection companies are stacking their services with Loan Application Monitoring — a brilliant feature that alerts you when a loan application is submitted in your name. Yes, this happens all the time, and it gives a whole new meaning to the term ‘loan shark.’

SSN Monitoring

Your social security number is the key to your identity. So you must protect this key with a robust monitoring service that scans millions (sometimes billions!) of data points looking for your SSN. If it’s found being used by anyone but you, you’ll be alerted immediately.

Updated January 8, 2026

copied!

Updated January 8, 2026

copied!